Artificial intelligence is the future. Even if you don’t come in contact with the marvels of AI in your day-to-day life, it has permeated our society and is making improvements from behind the curtain. And its applications are not just limited to tech. Manufacturing, supply chain, medicine, and even our social structures are experiencing subtle AI interventions.

Finance is no exception, and the most common example of AI in consumer finance that we see and experience is robo-advisors.

Robo-advisors are AI-driven and algorithmic financial advisors. They’ve made investment advice cost-friendly, smart, and mathematical.

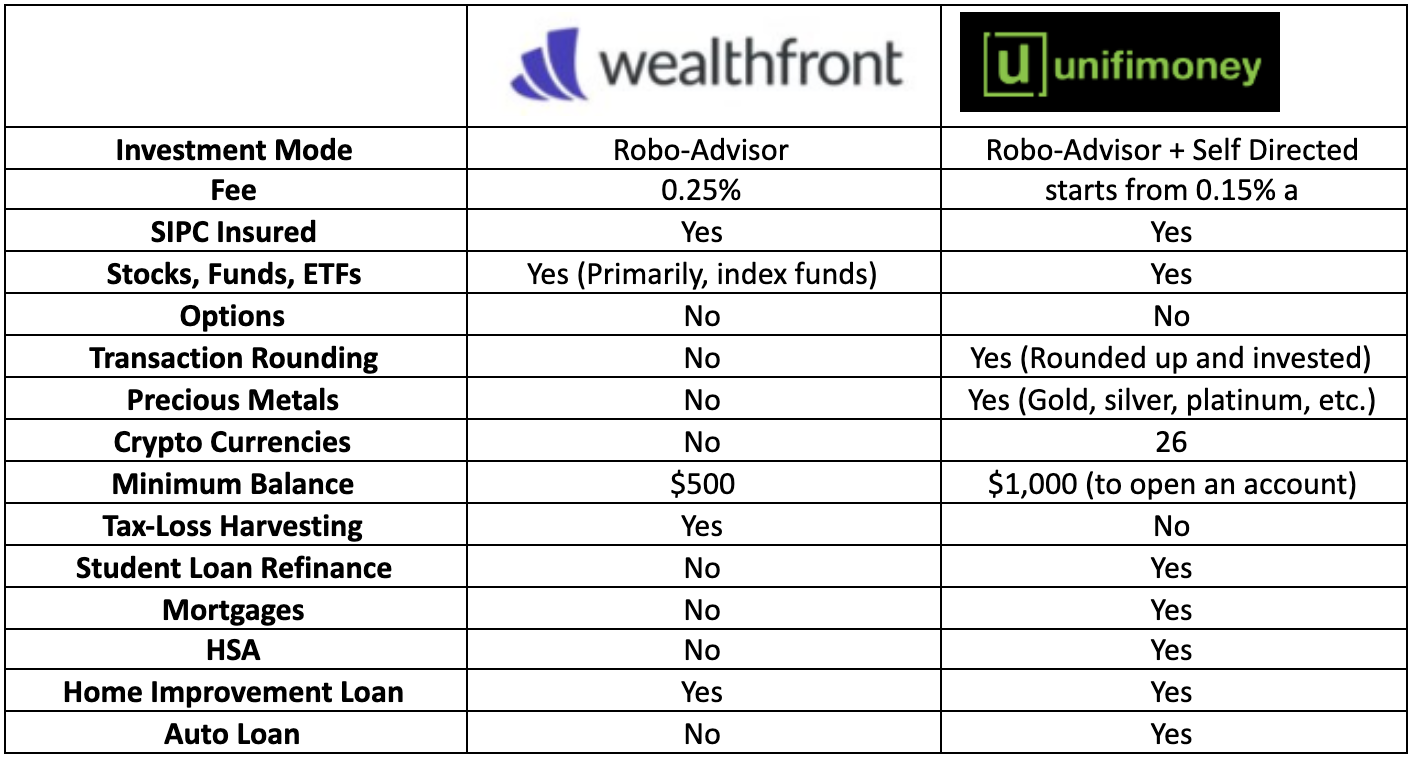

There are several robo-advisors available to investors; two of them are Wealthfront and Unifimoney. Let's see how these two fares against each other and which one can be the better fit for your investment needs.

Both Wealthfront and Unifimoney offer robo-advisors as part of their investment platform, but that’s not the extent of their features and services.

Wealthfront has been in the market since 2008 and has established itself as a dependable and reputable robo-advisor platform. The company has extended its service range and offers a cash account with a higher-than-market APY of 0.35%. The account also comes with no minimum balance and almost no fees. It also provides this account in conjunction with Green Dot banks, and it offers up to $1 million FDIC insurance.

Another feature that some users might find attractive is its portfolio line of credit, which essentially lets you borrow against your investment portfolio.

Unifimoney is relatively new to the banking and investing industry. It's a full-service neo-bank that offers a powerful investment platform and not just a robo-advisor that diversified its product and service portfolio. That's a significant distinction. It offers a hybrid account that acts as your savings and checking account and your brokerage one. This makes it a lot easier to handle and operate since you don't have to move funds around three different accounts. It’s currently offering an APY of 0.2%. Its deposits are backed by the UMB bank and are up to $750,000 FDIC insured.

Unifimoney offers a full suite of services that a bank would offer, making it significantly more than a robo-advisor.

There is a lot of overlap between the two platforms, but they also have their unique and differentiating features.

Wealthfront charges a flat fee of 0.25% annual advisory fee, whereas Unifimoney offers three tiers of robo-advisory, each with its own fee (charged annually):

Basic: 0.15%

Advanced:0.25%

Pro: 1%

The basic tier would be suitable for most retail investors. If you are starting with a portfolio of $100,000 growing at 8% a year, the below chart shows how your fees will progress in ten years.

(The amount you pay in fees would keep increasing with the increase in your portfolio size. Since Wealthfront fees are higher, you will end up paying significantly more over the years, than you would with Unifimoney)

Wealthfront Fees: $3,622

Unifimoney Fees:$2,173

In ten years, the difference in fees would be about $1,450. Wealthfront also charges fund fees that might vary between 0.06% and 0.13%.

The most significant difference between the two platforms is that unlike Wealthfront, which is purely a robo-advisory service, Unifimoney also allows you to direct your own trades. That can be a significant difference for those who understand the stock market or want to manage a part of their investment portfolio themselves.

Wealthfront focuses on a globally diversified portfolio of low-cost index funds (11 different asset classes) to maintain your portfolio and returns. The company's investment strategy (and its robo-advisor algorithm) is rooted in passive investment principles. One of the best features in Wealthfront's investment arsenal is its tax-loss harvesting. The company times the trades in a way that allows you to enjoy a lower tax bill. For portfolios up to $100,000, the tax-harvesting is done at the fund's level. But once a portfolio exceeds this threshold, the system starts looking into stock-level tax harvesting.

Investors with more extensive portfolios ($100,000 or more) experience other perks as well, like Risk Parity, which aims to enhance your risk-adjusted returns by following an enhanced asset allocation strategy. For investors with half a million or more in investments, Wealthfront offers Smart Beta. These strategies are part of Wealthfront’s PassivePlus investment strategies suite.

Unifimoney’s major edge over Wealthfront is its ability to self-direct investments and a more comprehensive range of assets. By adding precious metals and crypto into the mix, you can improve your portfolio's odds of outperforming the market, especially during turbulent times and recessions. Thanks to an advanced AI and the robo-advisor tiers that Wealthfront offers, you have access to the top-of-the-line features and AI, regardless of your portfolio's size (if you are willing to pay extra). You can leverage the full-power of Unifimoney’s robo-advisor to expedite the growth of your investment portfolio.

There are other differences, as well.

Both Wealthfront and Unifimoney offer very different services. Unifimoney is part of a new breed of money "super-apps" acting as a fully integrated one-stop-shop for high-earning professionals. It replaces the need for multiple apps and banks. Wealthfront is still primarily a mono-line Robo advisor, although likely to continue to add services over time.

However, the robo-advisory algorithms, focus, asset mix, and tax handling of the two platforms are drastically different. If you strictly want to stick to robo-advisors, you may want to look at the performance, projections, and specifics of the two platforms' robo-advisor functionality. But if you want something more comprehensive, Unifimoney might be the better choice.

The above does NOT constitute an offer, solicitation of an offer, nor advice to buy or sell specific securities. The opinions listed above are not the opinions of Unifimoney Inc. or Unifimoney RIA, Inc. but represent the opinions of independent contributors. These contributors may or may not hold positions in the stocks discussed. Investors should always independently research any stocks listed and form their own opinions, while recognizing that any investments made may lose value, are not bank guaranteed and are not FDIC insured.